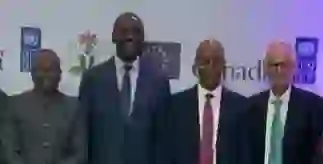

The Federal Government, in collaboration with the United Nations Development Programme (UNDP), has launched a new initiative aimed at improving Nigeria’s sovereign credit rating to reduce borrowing costs, attract foreign investment, and strengthen the country’s economic standing.

The initiative was unveiled during a High-Level Debriefing Meeting on the Credit Ratings Needs Assessment Mission for Nigeria held in Abuja.

Speaking at the event, the Minister of Finance and Coordinating Minister of the Economy, Mr. Taiwo Oyedele, said Africa continues to face significantly higher borrowing costs due to what experts describe as the “African Premium”—a perception-driven risk factor that costs the continent an estimated $74.5 billion annually in additional financing expenses.

Represented by the Permanent Secretary (Special Duties) in the Ministry of Finance, Mr. Mohammed Sanusi, Oyedele said the Federal Government is committed to ensuring that Nigeria’s sovereign credit ratings accurately reflect the country’s economic progress and reform efforts.

He explained that rather than focusing on perceived shortcomings in the global financial system, the government is strengthening institutions, improving engagement with international credit rating agencies, and enhancing the credibility of economic data.

According to the minister, recent positive assessments from Moody’s, Fitch Ratings, S&P Global Ratings, and the International Monetary Fund (IMF) indicate growing confidence in Nigeria’s economic reforms.

He stressed that achieving stronger sovereign ratings goes beyond economic performance, noting that data quality, policy consistency, institutional coordination, transparency, and effective communication with rating agencies are equally important.

“Our objective is not simply to secure better ratings, but to ensure that Nigeria’s credit profile reflects the resilience of our economy and the opportunities created by ongoing reforms,” he said.

Also speaking, the UNDP Chief Economist for Africa, Raymond Gilpin, noted that declining global development assistance has made affordable access to capital increasingly important for African countries.

He explained that many African nations have graduated to middle-income status, limiting their access to concessional financing even as funding requirements for infrastructure, technology, poverty reduction, and sustainable development continue to rise.

Gilpin said sovereign credit ratings play a critical role in shaping investor confidence and determining the cost of raising funds in international financial markets.

He revealed that the Africa Credit Ratings Initiative, established by the UNDP in partnership with the African Development Bank (AfDB), United Nations Economic Commission for Africa (UNECA), Africa Centre for Economic Transformation (ACET), and the African Peer Review Mechanism (APRM), is designed to help African governments improve engagement with credit rating agencies, strengthen institutional capacity, and enhance the quality of economic data.

As part of the programme, the UNDP recently sponsored senior government officials from 11 African countries to study how the Philippines successfully improved its sovereign credit rating from non-investment grade to investment grade.

Gilpin identified weak data management and limited transparency as key challenges affecting many African countries, saying these shortcomings often lead to subjective assessments by international rating agencies.

He expressed optimism that Nigeria’s ongoing reforms and recent improvements in sovereign ratings have positioned the country on the path toward achieving investment-grade status, a development expected to boost investor confidence and lower borrowing costs.

The Canadian High Commissioner to Nigeria, Pasquale Salvaggio, also reaffirmed Canada’s commitment to expanding economic relations with Nigeria.

He disclosed that non-oil trade between both countries has increased by 50 percent, making Nigeria Canada’s second-largest trading partner in Africa. He added that Canada would continue working with Nigerians in the diaspora to encourage greater investment in the country’s economy.

The meeting concluded with stakeholders identifying practical measures to strengthen Nigeria’s engagement with international credit rating agencies, improve institutional capacity, and ensure that the country’s sovereign ratings accurately reflect its economic reforms and long-term growth potential.

READ ALSO:

- Founder of All Christians Fellowship Mission, Rev. William Okoye, Dies

- Senate Approves FRSC Bill Proposing ₦50,000 Fine for Hawking, Preaching in Commercial Buses

- FG, UNDP Launch Initiative to Strengthen Nigeria’s Credit Rating, Reduce Borrowing Costs

- Army Arrests 24 Foreign Nationals in Raid on Suspected Hideout in Lagos

- The Rise and Rise of Kadri Obafemi Hamzat: The Quiet Reformer Shaping Lagos’ Future

{kind=link}